The Importance of an Emergency Fund

Savings, emergency fund, slush money, rainy day fund – there are so many names for what is essential the same thing. Everyone knows you should have some savings, yet 58% of Americans have less than $1,000 socked away. Usually, that’s because you’re thinking: Why should I save for a possible future event when I have so many current actual expenses to fund?

The term “emergency fund” is a little misleading. It assumes the possibility of an event derailing your monthly finances. For example:

You may end up in the Emergency Room sometime this year, but history has shown that you probably won’t.

You may need to repair your car, but it hasn’t broken down in two years.

You may need to pay for plumbing repairs, but for the past two or three years, that hasn’t been necessary, so why worry enough about it to throw money towards an invisible problem?

It’s a little elementary, but let’s break down how an emergency is defined: an “unforeseen combination of circumstances that calls for immediate action.” When we save for an emergency, we are mentally categorizing funds for an unforeseen expense.

Here’s the thing: car repairs, plumbing, school costs, medical bills… all of these things are sporadic, but they are not unforeseen. These are normal costs of living and owning assets such as homes and cars.

When we think of emergency savings as a potential expense instead of a guaranteed one, we are setting ourselves up for a scary situation that can really affect our financial lives. Emergencies in the way we typically think of them aren’t unexpected – they’re inevitable, and we have to plan accordingly.

Many debt advisors such as Dave Ramsey will harp on the concept of saving $500-1,000 first, then focusing on paying debt. Many of us completely ignore step one and go straight to the debt repayment process. “Why have money sitting there when it could be reducing my debt load?” you think. (I can’t even tell you the amount of times I have done this).

The answer is in the assumption of fixed monthly expenditures. The average individual will assume that even with some fluctuations their monthly costs will remain about the same. It ignores the very real possibility of sporadic maintenance and living costs.

A slush fund or some form of savings helps to cover the gaps when certain costs rise throughout the year. You can get a baseline on what your fund should look like by examining your monthly expenses, or by using the standard 10-20% of your earnings. Personally, I would add to that amount if you have a lot of assets that require upkeep – an older home, two or three cars and/ or an older model on its way out, perhaps a camper or additional home.

“When in doubt, estimate expenses

higher and income lower. ”

To get my baseline, I take 1% of the value of every asset I own and put it in my yearly budget spreadsheet. At the end of the year when I’m reevaluating and planning for the next budget, I’ll adjust those expenses to the actual cost if they were higher. If they were lower, however, I leave them at 1%, because this matches my risk profile: When in doubt, estimate expenses higher and income lower.

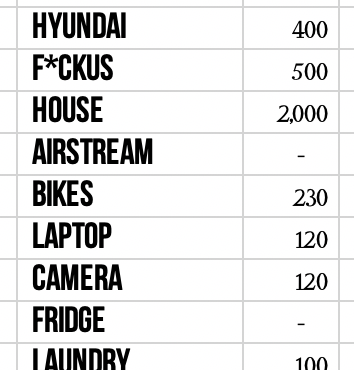

This is a small selection from my list. One car is newer and more expensive, but has lower yearly costs, so it stays about 1%. The other car is an older model that requires more upkeep, so it hovers around 8%. Our home is also at a higher percentage, because it was built in 1928 and we know we should plan to spend on major improvements yearly. Now, realistically, am I going to spend more than a $100 on maintenance for my camera? No. But I might buy another lens or memory card, and it’s nice to have planned for it in the budget. Worst case scenario, I have money set aside for some other unexpected cost. I don’t actually earmark this money specifically for this asset; rather, I take the total to use as my baseline for how much I should have in my sporadic expense fund. *see note below

I’m a total accounting nerd and would love if my life was taken over my many spreadsheets, but I get that others might consider this method to be, at best, intensive, and at worst, neurotic. If 3-6 months of expenses in savings works for you, go for it! I just like playing with my numbers to see the real costs of owning an asset on a yearly basis. It forces me to realize the actual cost of an item over its lifetime, instead of defaulting to its original sticker price.

However you choose to do it, the point of this exercise is to: think about the amount you personally feel comfortable having in savings, and to shift your thinking away from the traditional emergency savings trap.

By really assessing my unexpected costs yearly, I avoid panic and unnecessary worry. Every time we actively choose to avoid saving, we are risking derailment of our debt repayment plan. Saved money isn’t wasted money, and it definitely isn’t optional for the person trying to avoid additional debt or financial stress.

*I use Qapital to save for specific expenses. For instance, my husband and I knew we would be soon replacing our front door. After some research, we knew we would need $1,000. We started a joint savings fund on Qapital for this purpose. When our Great Dane took out the glass last week (she’s okay! The 91-year old door, however…), it was light work to pull the money and order the door. I put it on a credit card to reap the rewards, but paid it off immediately using that cash. Read my full review of Qapital later this week and get a $10 instant savings code. Read my promise to you about affiliated links.